FinTech companies are driving the development of new business models in the financial sector through platforms and ecosystems. Regulatory requirements are redefining the boundaries of the banking industry and are widening the scope of products and services. However, banks are still more strictly regulated and face barriers to innovation, whereas FinTechs operating in the B2B sector are typically highly agile technology players that operate outside of the regulated domain.

The COVID-19 pandemic has triggered further digitization in the financial sector. The number of physical interactions has decreased, and customers are increasingly accustomed to arranging their financial needs online, resulting in changing customer expectations. In addition, FinTech banking companies are starting to obtain full banking licenses. Some examples include digital-only banks like N26, Adyen, Solarisbank and Revolut.

The changing regulatory landscape and digitization are driving greater connectivity between organizations and reshaping the financial ecosystem.

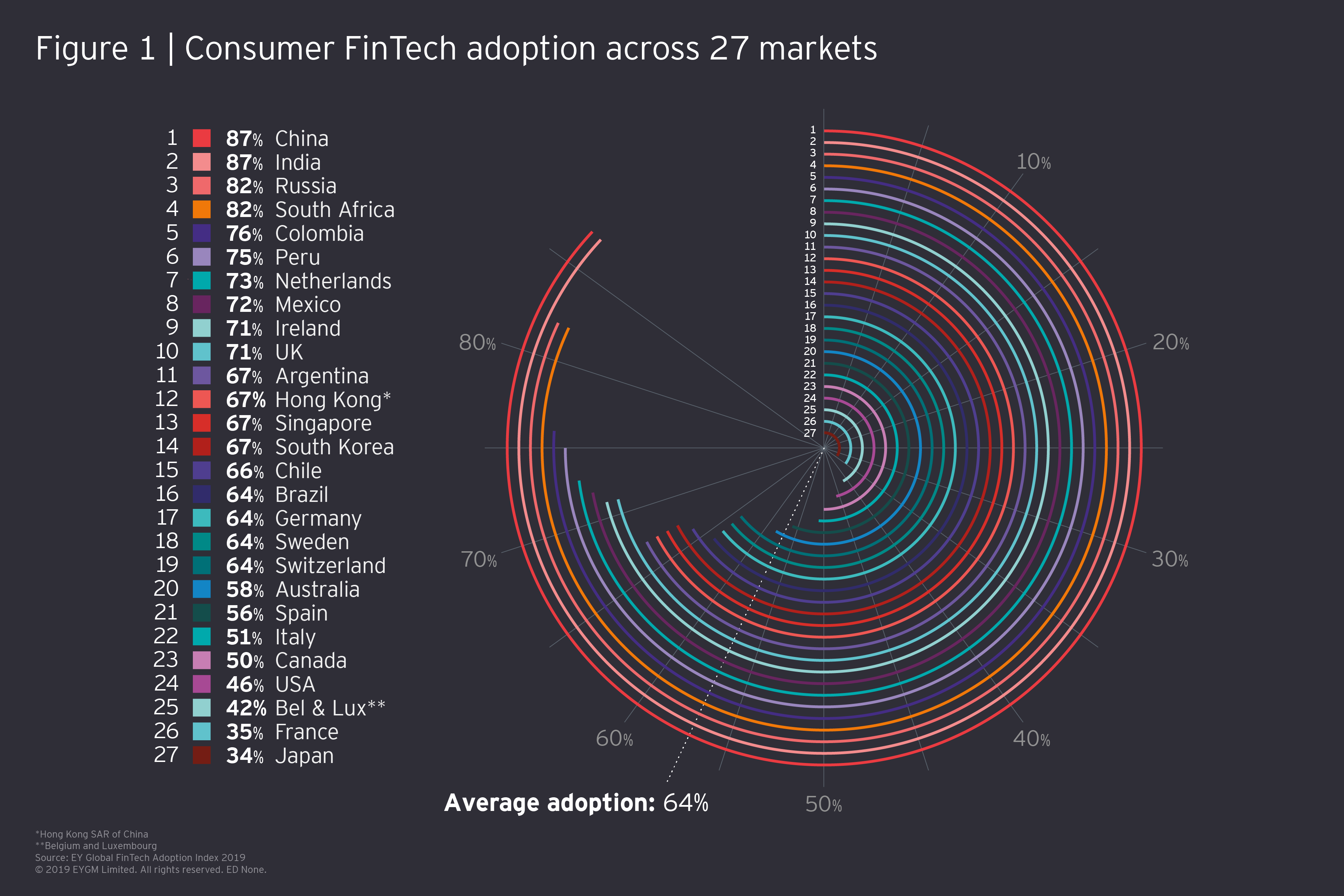

The adoption of FinTech services increased to 64% globally

Customer behavior is evolving along with global developments, resulting in customers’ increased willingness to use FinTech services. The EY FinTech Adoption Index shows that the adoption of FinTech services has increased globally from 15% in 2015 to 64% in 2019[1].

Within Europe, Dutch customers are embracing FinTech services the most, with an adoption rate of 73%2. This provides collaboration opportunities for FinTechs and banks in the Netherlands, as new services are likely to be embraced by Dutch customers. Solutions should be developed that meet the needs and expectations of Dutch customers.

Despite the increasing customer adoption rate, FinTech companies often struggle to form a solid client base. With high acquisition costs per customer, we see that many FinTech companies pivot into a B2B2C relationship or immediately focus on business services. This trend is also visible in EY’s monthly PSD2 data analysis, which shows that approximately 57% of the PSD2 licenses in Europe and the UK are focused on B2B (data up to January 2020). EY research on the Dutch FinTech sector shows that partnerships with financial institutions are viewed as the second greatest opportunity by FinTechs, after international expansion[2].

Figure 2. PSD2 licenses in Europe and the UK, January 2021

Multiple global developments create a clear need for collaboration

FinTech companies are eager to cooperate with banks for four reasons. First of all, banks generally have a more well-defined and stable client base. Next, a partnership, cooperation or collaboration with a bank is a stamp of trust that confirms the credibility of these FinTech services to the customer. A third reason is that banks tend to have bigger investment budgets that can provide a flow of capital to further develop FinTech services. Lastly, banks have a lot of internal know-how and knowledge in areas that FinTech firms can benefit from, such as legal and regulatory (e.g. Client Due Diligence) compliance and risk management.

Banks, on the other hand, have two main drivers to collaborate with FinTech companies. Customers have become increasingly used to a seamless digital experience and expect the same from their bank; a service few banks are able to provide (yet). Furthermore, due to the emergence of these one-stop-shops, FinTech companies have moved from being just a single service provider to providing a whole suite of services.

This shift to platform-based business models and an ecosystem set-up provides banks with various opportunities, if they decide to enter into these collaborations. Strategic partnerships have led to growth of the Banking-as-a-Service (BaaS) market, in which third parties can connect directly with the banks’ existing and well-regulated infrastructure, in order to provide a seamless customer experience. Moreover, regulatory possibilities, such as PSD2, give FinTech companies the possibility to directly integrate with traditional banks and share their technology to their mutual benefit.

Banks and FinTech companies cooperate in various shapes and forms, with the level of financial commitment as foundation

So, how to choose the right model for an effective collaboration? Unfortunately, there is not one right answer. We have identified important factors to consider before entering into a collaboration. This includes financial dependencies, brand and reputational aspects, responsibilities, operational dependencies (e.g. level of integration versus separation) and the level of involvement from management.

Many FinTech partnerships are based on financial commitments, for example via venture funds, mergers and acquisitions, varying from minority stakes to full acquisitions. 2019 was a record year in terms of merger and acquisition activity for the whole FinTech sector. After a promising start in 2020, FinTech M&A activity slowed down considerably in March due to the impact of COVID-19[3]. Yet the structural catalysts of deal-making, such as the need to increase scale and add new capabilities remained in place. M&A deals in 2020 were mainly focused on direct investment in payments, RegTech, WealthTech and automation. Bank venture funds also narrowed the focus on technology innovations that add value to the core business lines of the bank.

With the rise of ecosystems, EY sees FinTech partnerships with no or little financial commitment more frequently. Banks are investing in incubation or acceleration programs to engage with FinTech companies at an early stage. Increasingly, they invest in innovative collaboration models, based on reference and licensing models. These models enable the banks to offer FinTech solutions via their own channels or are platform-based, by referring to FinTech offerings on the bank’s platform or by offering white labeled FinTech solutions under the bank’s brand via a license structure. Besides the increase in offering FinTech services and products, banks are also increasing the in-house development of financial technologies and digital service offerings via innovation centers and labs, to be distributed via their own- or third-party platforms.

Key challenges for an effective collaboration are cultural gaps, getting the bank ‘grade’ ready and scaling and legacy from a technological perspective.

While the opportunities for collaboration and M&A in the FinTech landscape are numerous, both banks and FinTech companies perceive engaging in such partnerships to be very challenging. Key challenges are related to:

- Culture: One of the biggest challenges to collaboration is the gap between FinTechs’ innovative and entrepreneurial mindset and way of working versus the more risk-averse and traditional culture of incumbent players.

- Bank ‘grade’ ready: Having the appropriate controls, processes and policies in place to pass bank assessments on compliance, legal, risk and procurement level, can be challenging and very time consuming. After facing these hurdles, FinTechs also have to deal with various challenges related to sales and marketing. It is not uncommon to have long timelines (>18 months) for developing a POC from Lab to Live, which is a constraining factor for FinTech companies.

- Scaling & legacy: Many banks have large legacy IT platforms that need to be updated and maintained to conform to changing regulations, to support growth and cost optimization initiatives. At the same time they need to enable integration with emerging technologies at scale. This requires a shift from IT spend on maintenance of legacy systems to building the capability to run a scalable agile business model and the ability to integrate new financial technologies e.g. via the use of API’s.

EY experienced that an essential factor for effective collaboration is the need for coexistence and codependency. Both parties need to have clear collaboration incentives and the right sponsorship and stakeholder commitment to support the collaboration. Alignment between the incentives and strategic objectives of both parties is key to design effective partnerships around genuinely complementary capabilities. This form of collaborating mostly occurs through corporate venturing, leveraging capabilities from both parties and aligning incentives.

The success of a collaboration also depends on the flexibility and agility in business and IT as well as internal process maturity to adopt and implement new technologies. Stakeholders from these different domains should be involved from the start.

From the bank’s perspective, establishing a central innovation team that drives the activation, with linkage into different business units, ensures that the FinTech becomes integrated in the right place with the right support.